No matter what you do or where you are, every independent human need to manage their own finance. Minimum book keeping knowledge everyone should know, it is a life skill.

Financial accounting is not just for accountants, it’s a fundamental skill that empowers individuals to make informed decisions, whether in their personal lives, careers, or business endeavors.

Most avoid to dig into basics of financial accounting because of:

- Perceived Complexity

- Assumption of Irrelevance

- Overreliance on Professionals

- Fear of Making Mistakes

- Negative Past Experiences

Despite these challenges, it’s important to recognize the benefits of overcoming these barriers and developing a basic understanding of financial accounting. Financial literacy is an empowering skill that can enhance decision-making, improve financial well-being, and contribute to overall success in personal and professional life.

Financial domain jargons like Debit and Credit also created panic for average people and creates confusion. We will not go into those domain specific jargons in this excersise.

Let’s start with some basics to remove the fear or perceived complexity about accounting.

- Accounting at it’s simplest form, can be done with just addition and subtraction (+/-) only. No other form of complex calculation is required.

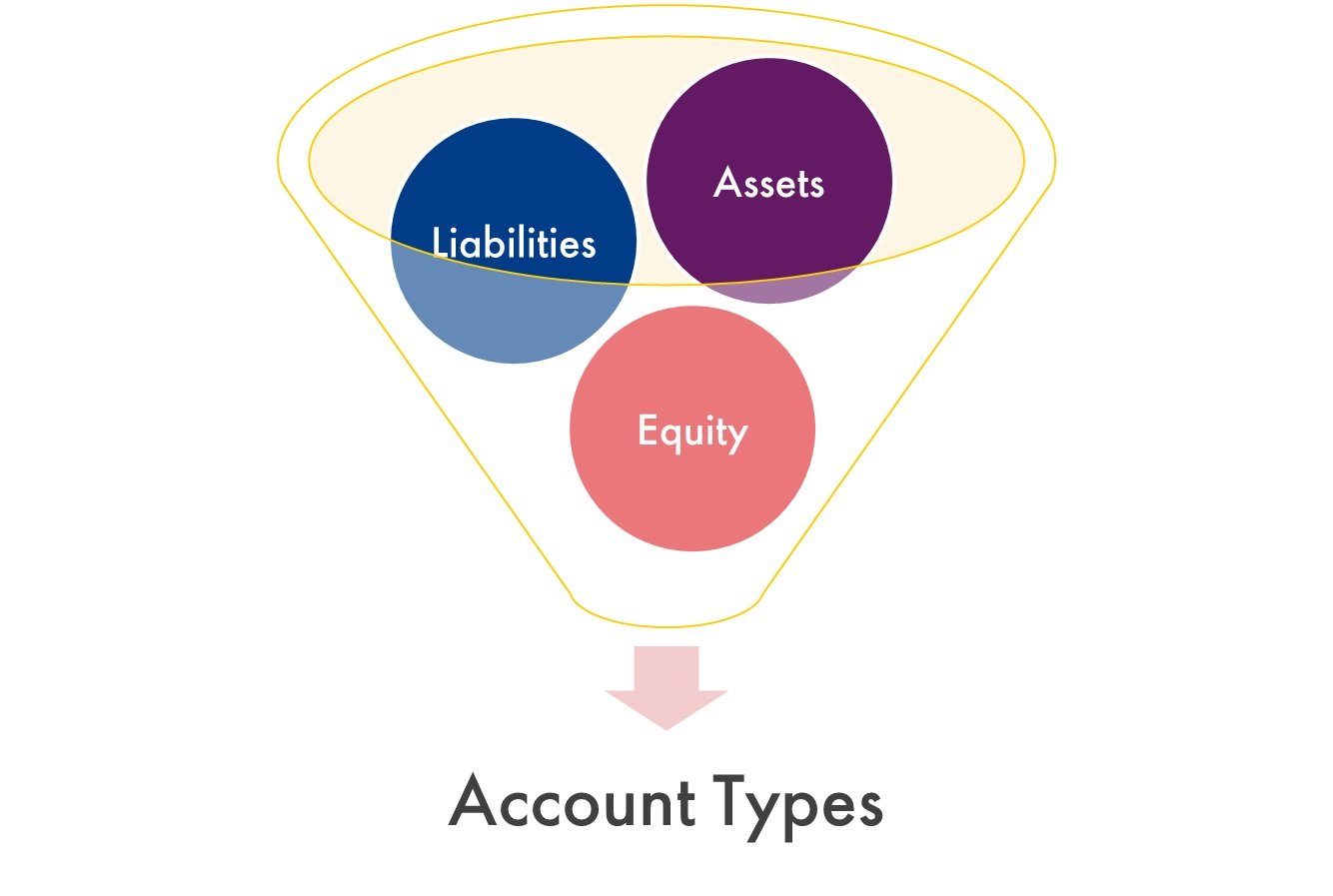

- Any type of financial transaction can be classified in simple three account types (Assets, Liabilities and Equity).

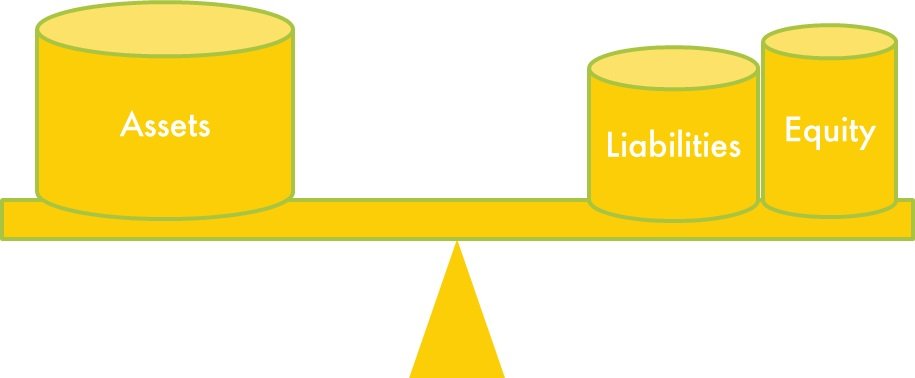

- The beauty of double entry accounting is that it always balances. In other word, the total sum of a transaction should always be ZERO as there are positive numbers and negative numbers involved.

- That all you need to know to be an accounting book-keeper. Surprised! Yes indeed, it is that simple.

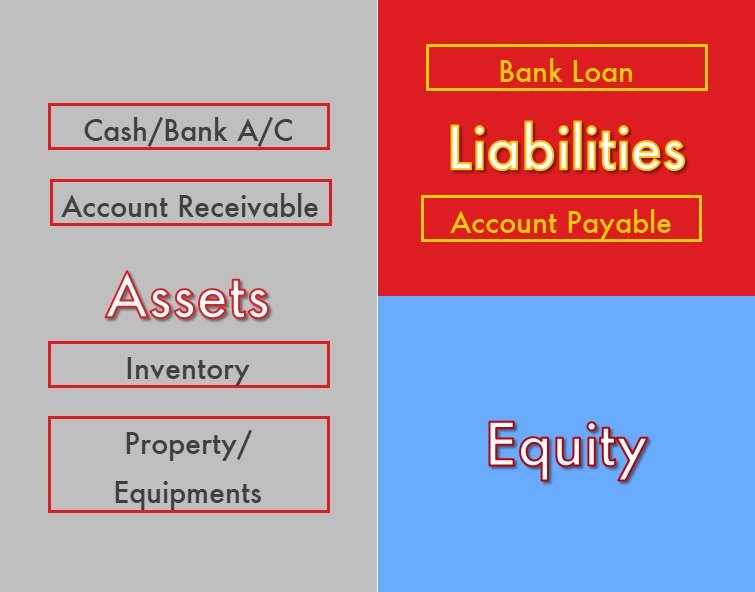

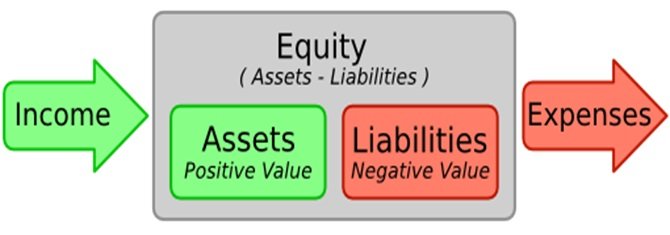

The three account type and their relationship

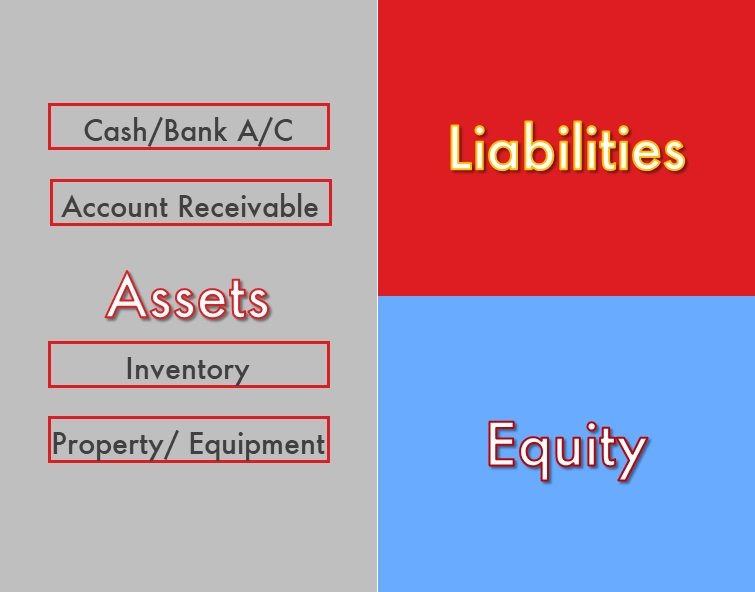

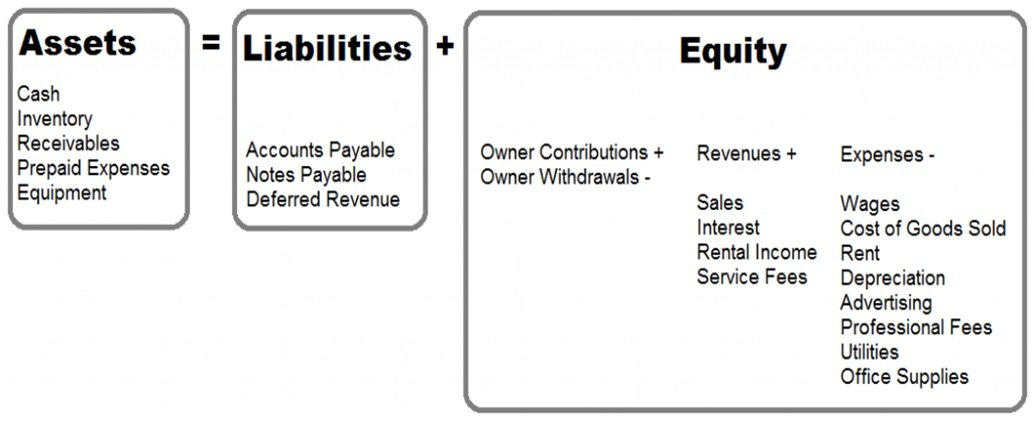

- Assets: Anything which can be converted to cash in future. (Cash at hand/Bank A/C, Stock, Property etc.)

- Liabilities: Anything which needs to be paid back in cash, kind or service in future, anything you owe to someone. (Bank loans, credit card dues, money received in advance)

- Equity: Balance amount retained from business after paying all expenses and dues, your own contribution of fund to start a business

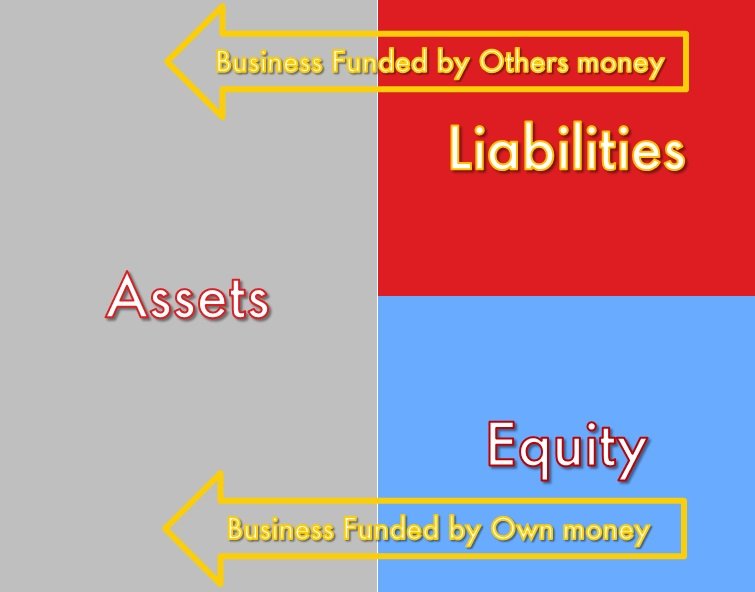

Only one equation to remember : – Assets = Liabilities + Equity.

Keeping this in mind the above rule all the below formulas as also true :

- Equity = Assets – Liabilities

- Assets = Liabilities + Equity

The three categories of accounts

1. What are Assets?

In financial accounting, assets are resources that a company or an individual owns or controls, and which are expected to provide future economic benefits. Assets can be tangible or intangible and are typically categorized into two main types: current assets and non-current assets.

Current Assets: These are assets that are expected to be converted into cash or used up within one year or the operating cycle of the business, whichever is longer. Examples include:

- Cash and Cash Equivalents: Currency, bank accounts, and short-term investments.

- Accounts Receivable: Amounts owed to the company by customers for goods or services sold on credit

- Inventory: Goods held for sale in the normal course of business.

- Prepaid Expenses: Payments made in advance for goods or services to be received in the future.

Non-Current Assets (or Fixed Assets): These are assets that are expected to provide economic benefits beyond the current accounting period. Examples include:

- Property, Plant, and Equipment (PP&E): Land, buildings, machinery, and other physical assets used in business operations.

- Intangible Assets: Non-physical assets without a tangible form, such as patents, copyrights, trademarks, and goodwill.

- Investments: Long-term investments in stocks, bonds, or other securities.

- Long-term Receivables: Amounts expected to be received after one year or more.

In summary, Anything which has a value, or that can be converted to cash is an Asset.

- Your Bank Account is an Asset.

- Someone owes you money (Account Receivable).

- Inventory, something you can sell or use in production to sell, to convert to cash.

- If you hold any property or equipment, which can be used to manufacture inventory or sold for cash.

- Assets can be of two sub-category:

- Current Assets : High liquidity items like, Cash at Hand, Bank A/C, Inventory etc.

- Fixed Assets : Low liquidity items like, Real Estate Property, Equipment, Plant & Machineries, Inventory etc.

2. What are Liabilities?

In financial accounting, liabilities are obligations or debts that a company or an individual owes to external parties. Liabilities represent claims on a company’s assets and can be categorized into two main types: current liabilities and non-current liabilities.

Current Liabilities: These are obligations that are expected to be settled within one year or the operating cycle of the business, whichever is longer. Examples include:

- Accounts Payable: Amounts owed to suppliers for goods or services purchased on credit.

- Short-term Loans: Borrowings that are due to be repaid within one year.

- Accrued Liabilities: Unpaid expenses that have been incurred but not yet paid, such as wages and utilities.

- Current Portion of Long-Term Debt: The portion of long-term debt that is due to be repaid in the coming year.

Non-Current Liabilities (or Long-Term Liabilities): These are obligations that are not expected to be settled within the next year. Examples include:

- Long-Term Loans: Borrowings with a maturity period of more than one year.

- Bonds Payable: Long-term debt securities issued by a company.

- Deferred Tax Liabilities: Taxes that are expected to be paid in future periods.

- Pension Obligations: Future payments related to employee pensions.

In summary, Any amount you owe to someone, or you need to pay back later.

- Any type of loans are liabilities.

- Suppliers to be paid (Account Payable).

- Salary taken in advance, for which your future income is reduced.

- Liabilities can be of two sub-category:

- Current Liability : Items which need to be paid back immediately within a year.

- Long-Term Liability : Items that can be paid back over multiple years, like Home Loan, Car Loan Etc. Long-Term Liabilities are also called Long-Term Debts.

3. What is Equity?

In financial accounting, equity refers to the residual interest in the assets of an entity after deducting liabilities. It represents the ownership interest of the shareholders in a company. Equity is often referred to as shareholders’ equity or owner’s equity and is a key component of the balance sheet.

It is also to be noted that unlike Assets or Liabilities, which are accounts to hold amounts. Equity is not an account to hold amount, We cannot treat Equity like a Bank account or a Loan account which holds assets/liabilities, rather it is an intangible entity to represent a calculated figure to indicate the value of the business. In other words, it is a mathematical representation of the owner’s interest in the business and nothing more.

(bit abstract? But don’t worry, we will clear it up later)

Equity is calculated using the following formula:

Equity = Assets − Liabilities

This equation demonstrates that the equity of a company is the difference between its total assets and total liabilities. Equity is further divided into several components:

Common Stock: This represents the par value of shares issued to shareholders.

Retained Earnings: This includes the cumulative net income earned by the company minus any dividends paid to shareholders. Retained earnings are reinvested in the business to support growth or reduce debt.

Additional Paid-in Capital: This accounts for any capital contributed by shareholders in excess of the par value of the common stock.

Treasury Stock: This represents shares of a company’s own stock that it has repurchased from the open market. Treasury stock is subtracted from the total equity.

Revenue: Well revenue is also the leftover of balance amount after paying all others. Intuitively we can feel that revenue do includes Income and Expenditure. We will look into it in details later, but for the time being let’s consider Revenue Expenditure and Income are sub category of Equity.

- Revenue Expenditure: Revenue expenditure refers to the funds a company spends on its day-to-day operational activities to maintain and run the business. These expenditures are incurred to generate revenue in the current accounting period and are not used for acquiring long-term assets. (Yes, there is also something called Capital Expenditure, which is different that Revenue Expenditure).Revenue expenditures are typically recurring and are charged against the company’s income in the period in which they are incurred. Examples include expenses for salaries, utilities, rent, repairs, and other costs necessary for daily operations.

- Income: Income, in accounting, represents the funds earned by a business through its primary operations, sales of goods or services, or other activities. It contributes to the company’s overall revenue.Income is generated through various sources, such as sales revenue, interest income, rental income, and fees for services rendered. It is a key component in determining a company’s profitability.

In summary, Revenue Expenditure encompasses the day-to-day costs incurred to keep a business operational. Income, on the other hand, represents the funds generated by the business through its operational and other activities. We can also say the any transaction that is reducing the Income is Revenue Expenditure, I other words negative income is revenue expenditure.

Balance amount retained from business after paying all expenses and dues:

- Your own contribution of fund to start a business or Withdrawal of fund from business.

- Your Revenue = Income – All Expenditure

- For the time being let’s limit our explanation of Equity as a combination of Owner’s Contribution/Withdrawal of the fund and Revenue(Income/Expenditure).

- Positive (+ve) Revenue are Income, and Negative (-ve) Revenue are Expenditure.

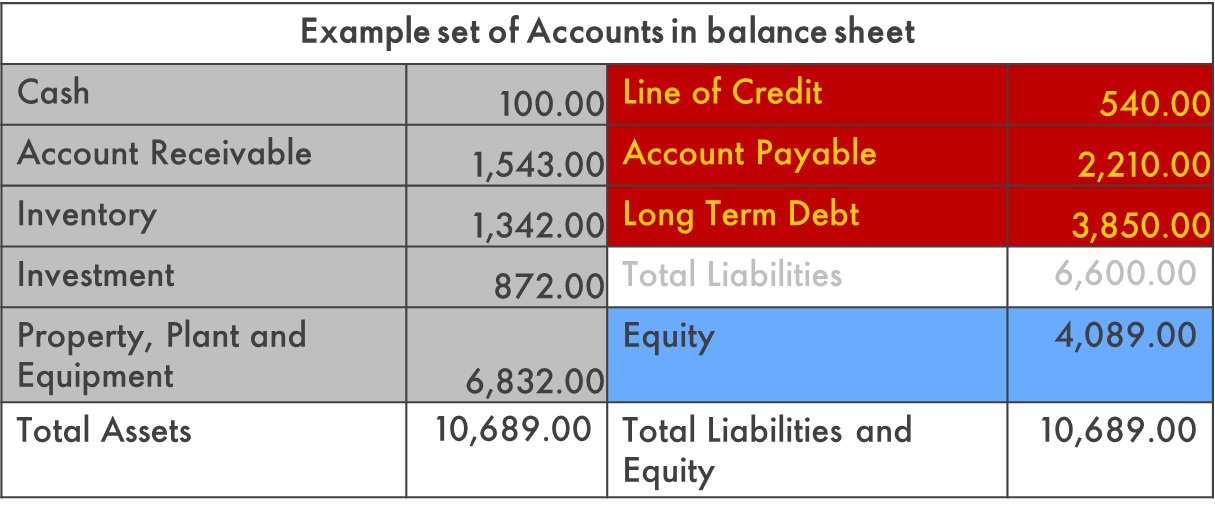

Example to understanding the concept of Equity

Let’s have a look into the example below:

All assets are on right hand, with total asset value of $ 10,689. But we are not entitled to this full amount we owe to other people money, for some of these Assets.

We have few liabilities of total amount $ 6,600.

We have a residual amount of $ 4,089 as equity. Which is the total amount we owe to others. This Equity amount represents the value of owner’s interest in the business. It not a bank account it is a mathematical representation of owner’s interest in the business.

In case the owner incurred loss in business for a year. In that situation the Equity amount will be negative. Please note, that the Total Assets can never be negative, but Total Equity can be negative.

So what are the things that can influence the Equity?

- It is important to understand how much money we are making from the business, for that there are statement of change in Equity.

- Equity can be Influenced/Changed, by two ways.

- Transactions on account of Revenue (Income & Expenses).

- Transactions on account of Capital (Owner’s Contribution & Withdrawals).

- Equity is NOT an Account. It is a mathematical representation of residual value of interest the owner is having in the business.

- So, Equity account represents all the accounts for owner’s capital contributions/withdrawals (+/-) and Revenue (+/-) (Income/Expenditure) accounts.

Another way of looking at it

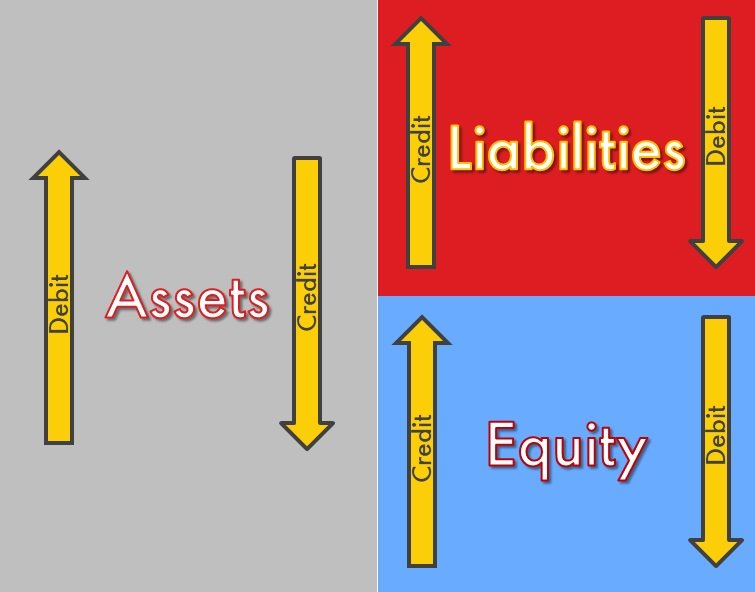

What about Debit and Credit! We haven’t mentioned DEBIT, CREDIT till now!

To avoid confusion, and associated stigma with the terms, non-accounting background people tries to avoid it. Just remember the below three point and you will never be confused about Debit/Credit.

- Debit/Credit is used to increase or decrease values in accounts, depending on which type of accounts are in question.

- For Asset accounts we use Debit to Increase value, Credit is used to Decrease value.

- However, it is reverse for Liabilities and Equity, which means, for both Liabilities and Equity accounts, we use Credit to Increase value and Debit to Decrease values.

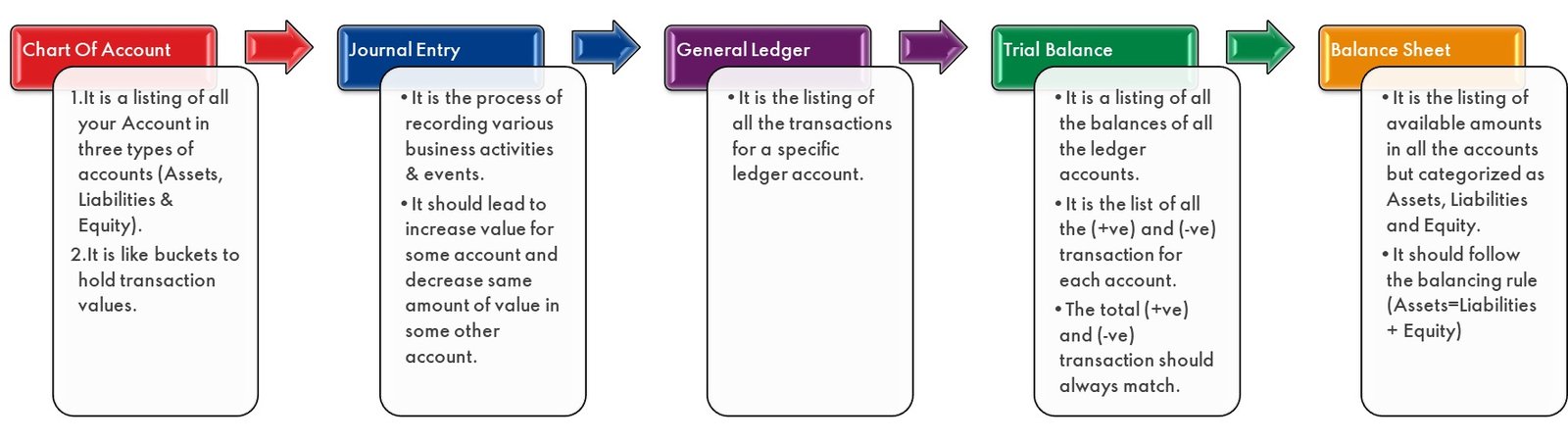

Mechanics of Accounting & Book-Keeping

Broadly there are five stages in any account system:

Chart Of Account (COA)

- It is a listing of all your Account in three types of accounts (Assets, Liabilities & Equity).

- It is like buckets to hold transaction values.

Journal Entry

- It is the process of recording various business activities & events.

- It should lead to increase value for some account and decrease same amount of value in some other account.

General Ledger

- It is the listing of all the transactions for a specific ledger account.

Trial Balance

- It is a listing of all the balances of all the ledger accounts.

- It is the list of all the (+ve) and (-ve) transaction for each account.

- The total (+ve) and (-ve) transaction should always match.

Balance Sheet

- It is the listing of available amounts in all the accounts but categorized as Assets, Liabilities and Equity.

- It should follow the balancing rule (Assets=Liabilities + Equity)

For the time being we will focus only on the two item “Chart Of Account” and “Journal Entry”, if we use an account tools, then the tool will take care of the other steps in the background.

1. Chart Of Accounts (COA)

A Chart of Accounts (COA) is a systematic listing of all the individual accounts used by an organization to record its financial transactions. It provides a structured framework for organizing and categorizing the financial activities of a business. The Chart of Accounts is a fundamental tool in accounting, helping to standardize the recording, classification, and reporting of financial information.

Chart of Accounts can be very simple with just the Account name and the associated account category (Assets/Liabilities/Equity/Income/Expenses) or it can be very complex for large multinational corporations, with many other attributes apart from Account Name and Account Category.

Key attributes of a Chart of Accounts include:

Account Numbers: Each account in the Chart of Accounts is typically assigned a unique number/name for easy identification and organization.

Account Titles: Descriptive names or titles that represent the nature of each account. For example, “Cash,” “Accounts Receivable,” “Sales Revenue,” etc.

Account Types: Accounts are classified into various types based on their nature, such as assets, liabilities, equity, income, and expenses.

Sub-Accounts: In some cases, accounts may have sub-accounts to provide more detailed breakdowns. For instance, “Utilities Expense” may have sub-accounts for electricity, water, and gas expenses.

Order and Hierarchy: The Chart of Accounts is often organized in a specific order or hierarchy, facilitating the efficient recording and reporting of financial transactions.

A well-organized Chart of Accounts is essential for accurate financial reporting, budgeting, and analysis. It helps financial professionals and stakeholders easily locate and understand specific financial transactions within the company’s records. The structure of the Chart of Accounts may vary based on the size and nature of the business.

- In Chart Of Account (COA), we identify the items we want to track during a period (mostly between 1 months to 1 year), which lead to some financial transaction.

- We can make it very high level of granularity.

- For example – Let’s say we want to track all travel expenses made by our staffs. We can have a single account as “Travel Expenses” or we can have employee wise travel expense accounts.

- But most important thing is to identify under which category these accounts should go. In this case, obviously “Travel Expenses” cannot be classified as an Asset account. “Travel Expenses” should be an expense account type.

- Chart Of Account (COA) is setting up various buckets for various transaction types.

- It is important to do it right, because we will be stuck with it for rest of the accounting period.

- Setting up Chart Of Account (COA) is almost an art. It needs skills, foresights, social and political understanding. It is possible that in some scenario, same account can be classified as Asset by one person, while other may classify it as liabilities.

- Chart Of Account (COA) can be a political tool, many financial reporting frauds uses COA to hide scams or mis-reports the financial health of company.

- We should take time and think through to create the COA. Most of the account heads are obvious and straight forward to classify as Assets/Liabilities/Equity.

This one of the most creative part in accounting and book keeping. What account is included and how they are categorized can be debatable, it can be political, also cultural.

Same account can be interpreted as Assets in some organization while others may categorize it as Liability. Chart of acount can be used creatively to manupulate auditor/share holders, hide frauds etc. We can have a separate article on this, but for this article it is out of scope.

2. Journal Entry

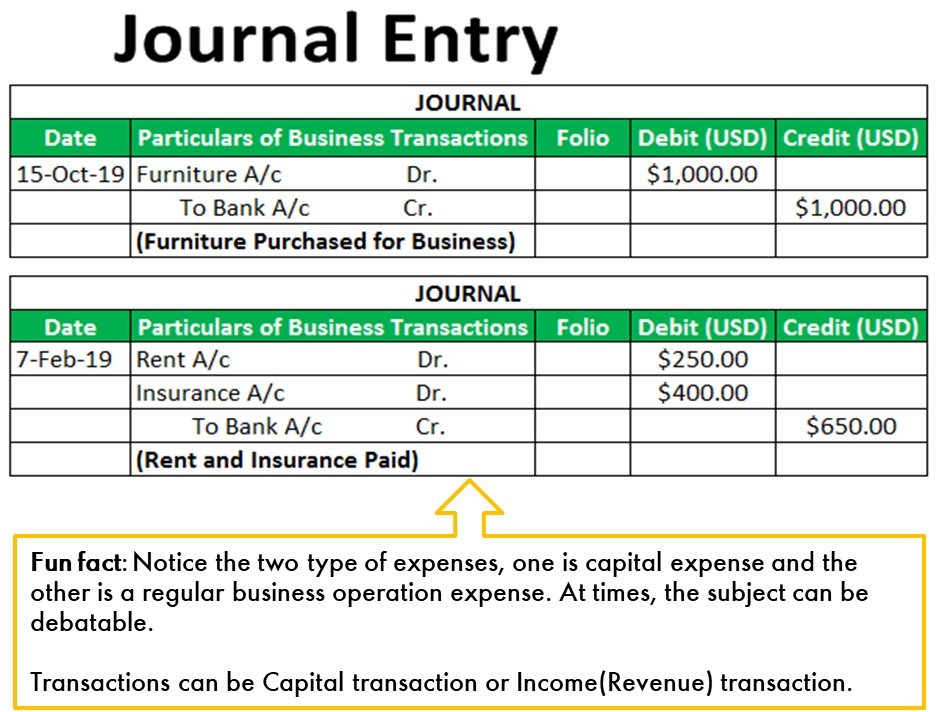

A journal entry in accounting is a method used to record a business transaction in the accounting records. It involves the chronological recording of financial transactions. Each journal entry consists of at least two parts: a debit and a credit. The total debits must equal the total credits for the entry to be balanced.

The process of making a journal entry involves three steps:

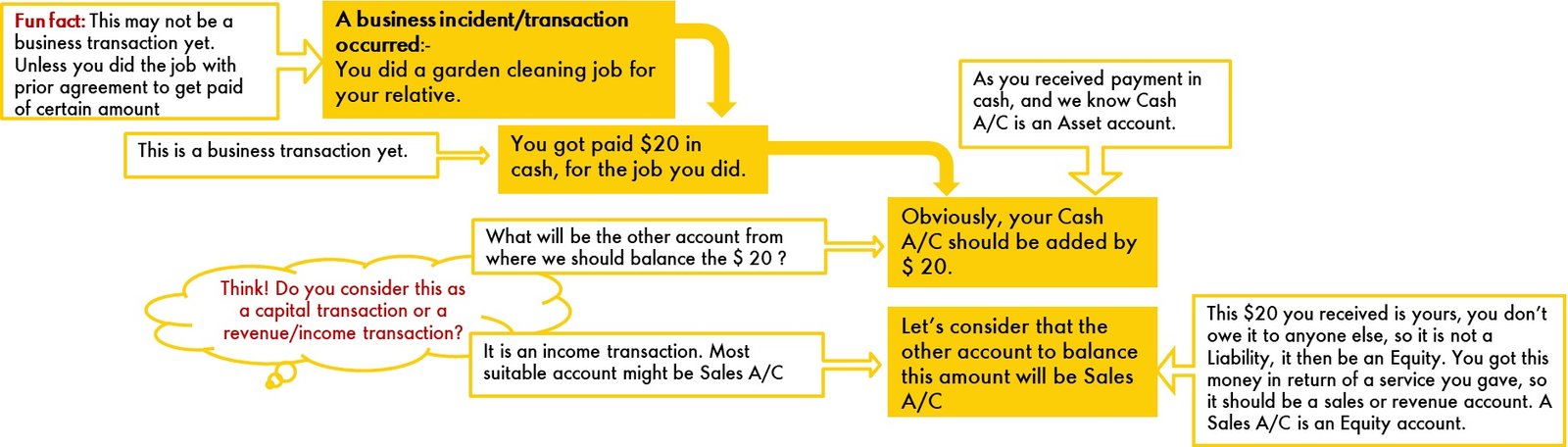

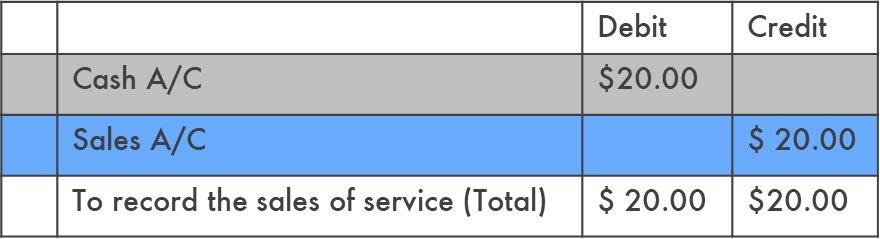

As we can see that at the core of journal entry there is a transaction or a business activity. And in a simplistic way, we can say, all transactions can be classified as Capital transaction or Income (Revenue) transaction. See the sample journal entry below:

Please note the debit/credit in the sample. Just understand that some amount is deducted from some account, while same amount should be added to some other accounts.

- Journal Entry is recording all type of business incidents/activities, like selling product, making payrolls, collecting receivables, buying inventory paying suppliers etc.

- A journal entry composed of an equal amount of (+Ve) and (-Ve) transaction and the respective accounts identifies between which the transaction happened.

- As it is recording of an activity, it should also have a Date of the incident and a clear description of the incident.

- And the (+Ve) and (-Ve) amounts should match in a transaction.

Let’s do a sample Journal Entry

Let’s consider a simple example. Suppose you did a garden cleaning job for your relative. And you got paid $20 in cash, for the job you did. Isn’t a business activity?

First step, we need to Analyse the transaction and Second step, to find out the suitable accounts and its category involved in this transaction.

Third step, is to aply the accounting rule (Assets = Liabilities + Equity).

- By default, all Assets are Debit A/C. Which means – All (+ve) amount in Assets are Debit balance. All (–ve) amount in Assets are Credit balance.

- By default, all Equity are Credit A/C. Which means – All (+ve) amount in Equity is Credit balance. All (–ve) amount in Equity are Debit balance.

If Debit/Credit is not your cup of tea? No need to worry.

- Please note we are simply increasing $20 to our Asset (Cash A/C) and we are also increasing to Equity (Sales A/C) and it is doing the balancing act.

- Because by default all Assets are Debit so we increase the cash amount.

- Similarly, by default all Equity are Credit so we also increase the sales amount.

To re-cap:

- Assets must equal Liabilities plus Equity (Assets = Liabilities + Equities).

- Total Debit must always equal Total Credit in a transaction.

- There is no such thing as one-sided Journal Entry.

- Every transaction must involve and adjust at least two accounts.

- Assets must have Debit Balances, and Liabilities must have Credit Balances

- Change in Equity must be reconciled by calculating Net Income and adjusting for owner’s contribution/drawings.